Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Lots of buyers are wondering: “Should I wait until rates come down before buying?” The answer depends heavily on how much you expect rates and home prices to move in the meantime. Here in South Snohomish / North King County the margins can get pretty thin. Using up-to-date numbers helps show why.

Current Rate Snapshot

-

30-year fixed mortgage rate: 6.29% per Mortgage News Daily. Mortgage News Daily

-

For comparison, many buyers have been using 7% as a benchmark “high rate” in past scenarios.

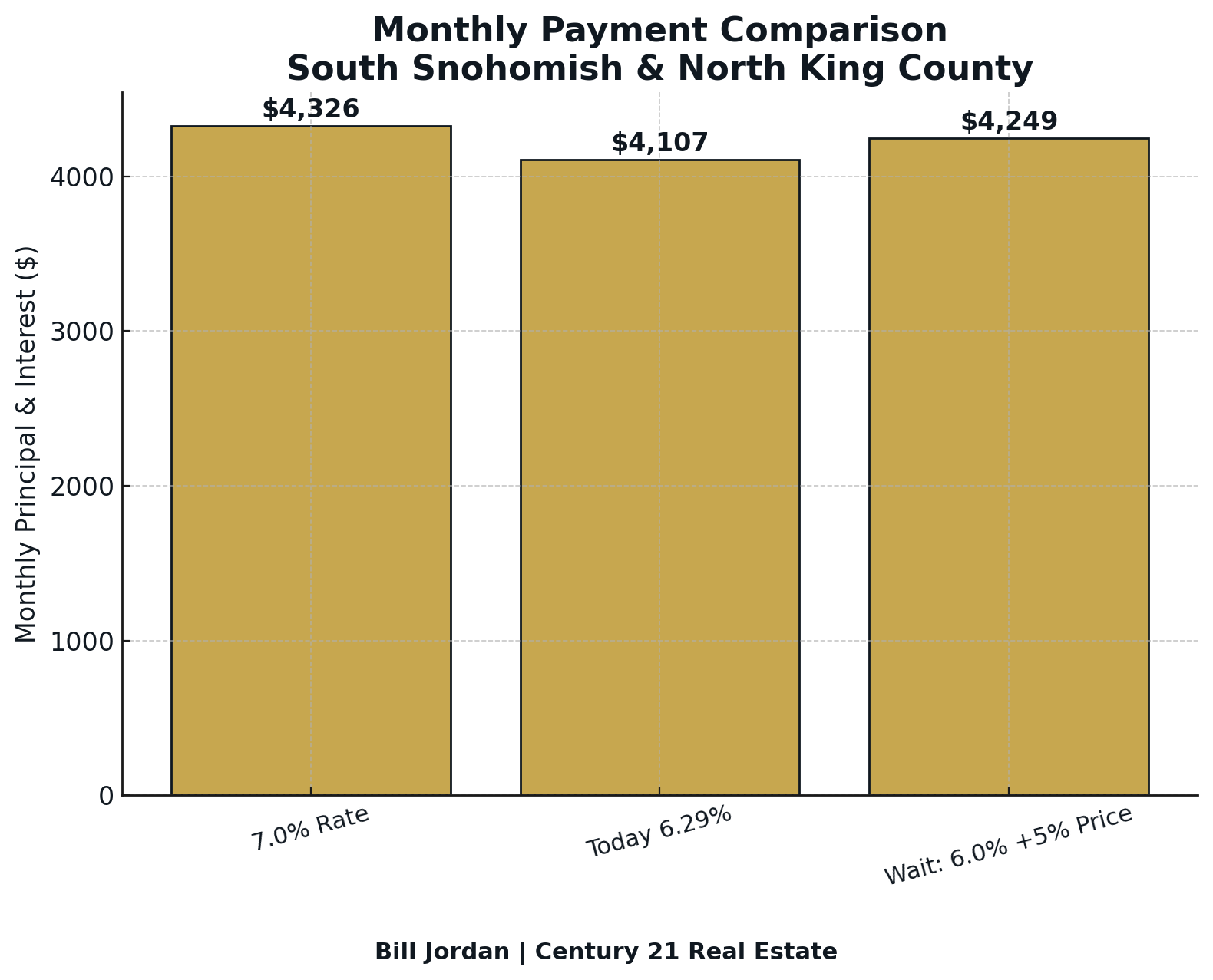

Example: $800,000 Home — Comparing 7% vs Today’s 6.29%

Let’s do the math for a typical scenario; adjust for real numbers so clients can see clearly what waiting might cost vs what it might save.

| Scenario | Home Price | Down Payment (20%) | Interest Rate | Monthly Principal & Interest* |

|---|---|---|---|---|

| A. Using “old high-rate” assumption | $800,000 | $160,000 | 7.00% | ~$4,326 |

| B. Using today’s rate | $800,000 | $160,000 | 6.29% | ~$4,107 |

*These are approximate monthly payments for principal + interest, not including taxes, insurance, maintenance, or HOA fees.

So in Scenario B vs Scenario A, you’re saving about $220 /month just from the lower interest rate, assuming price and down payment are the same.

But What If You Wait & Prices Go Up?

Waiting isn’t free. If you expect home prices to rise (which is reasonable in many parts of North King / South Snohomish), a rate drop might be partially or fully offset.

Let’s imagine that in the future:

-

Rate drops to 6.00% (from today’s 6.29%)

-

But home prices increase 5% in that period → price goes from $800,000 to $840,000

Then:

| Scenario | Home Price | Down Payment (20%) | Interest Rate | Monthly P&I* |

|---|---|---|---|---|

| C. Waited | $840,000 | $168,000 | 6.00% | ~$4,249 |

Compare Scenario B (buy now at 6.29%) vs Scenario C (wait, price up 5%, rate down to 6.00%):

-

Scenario B monthly ≈ $4,107

-

Scenario C monthly ≈ $4,249

That’s about $140/month more in the waiting scenario, plus a higher down payment.

Local Implications for Buyers

-

Today’s rate of 6.29% gives a noticeable benefit over a 7% rate, all else equal.

-

If you believe prices will increase by more than ~3-5% while rates drop slightly (to ~6.0-6.5%), waiting could cost more over time.

-

Sellers in many parts of King / Snohomish are more open to concessions now, which helps offset affordability pressures.

Bottom Line

If you find a home you like, buying now (even at 6.29%) likely beats waiting for slightly lower rates + higher prices. The savings in monthly payment might be modest, but the risk of higher purchase price often outweighs it.