Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Fear of a recession can feel paralyzing—should it stop you from buying or selling a home? Let’s break down what history and experts really tell us.

📊 What the Data Shows

A June 2025 survey by John Burns Research and Consulting and Keeping Current Matters found that 68% of prospective buyers or sellers are delaying their plans due to economic uncertainty

This hesitation often stems from two assumptions:

-

Mortgage rates will drop during a recession.

-

Home prices will follow suit.

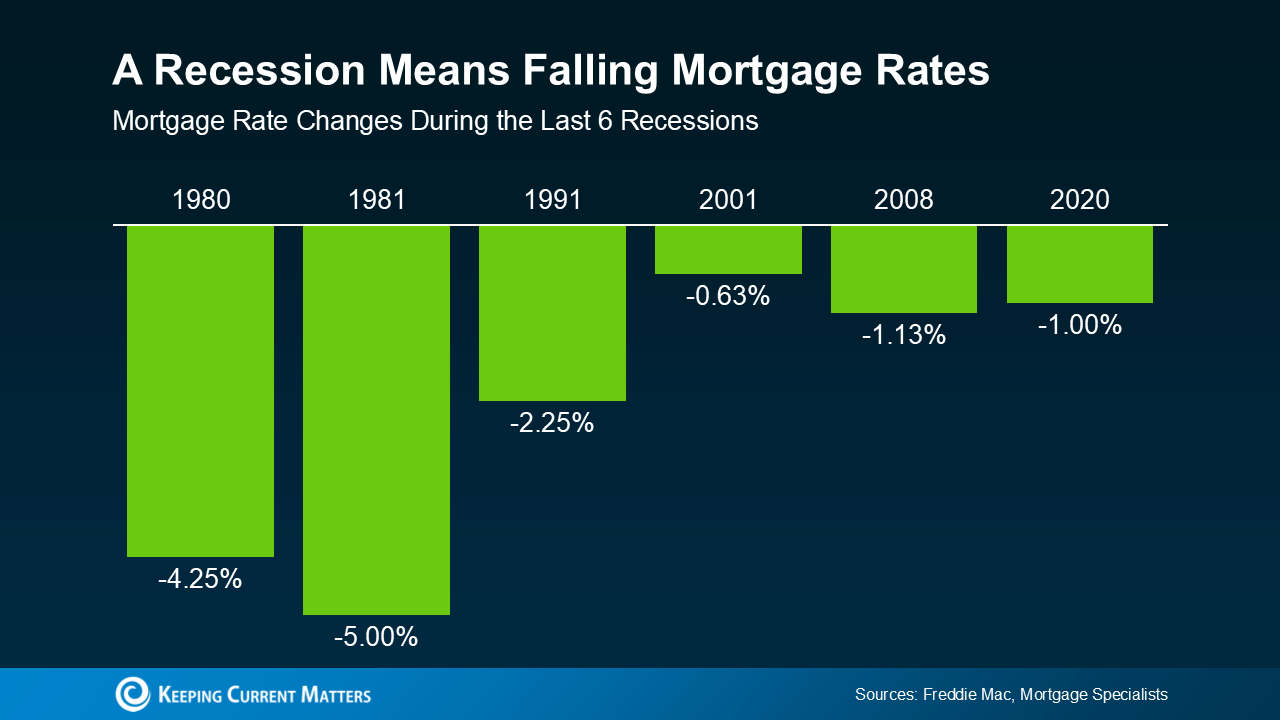

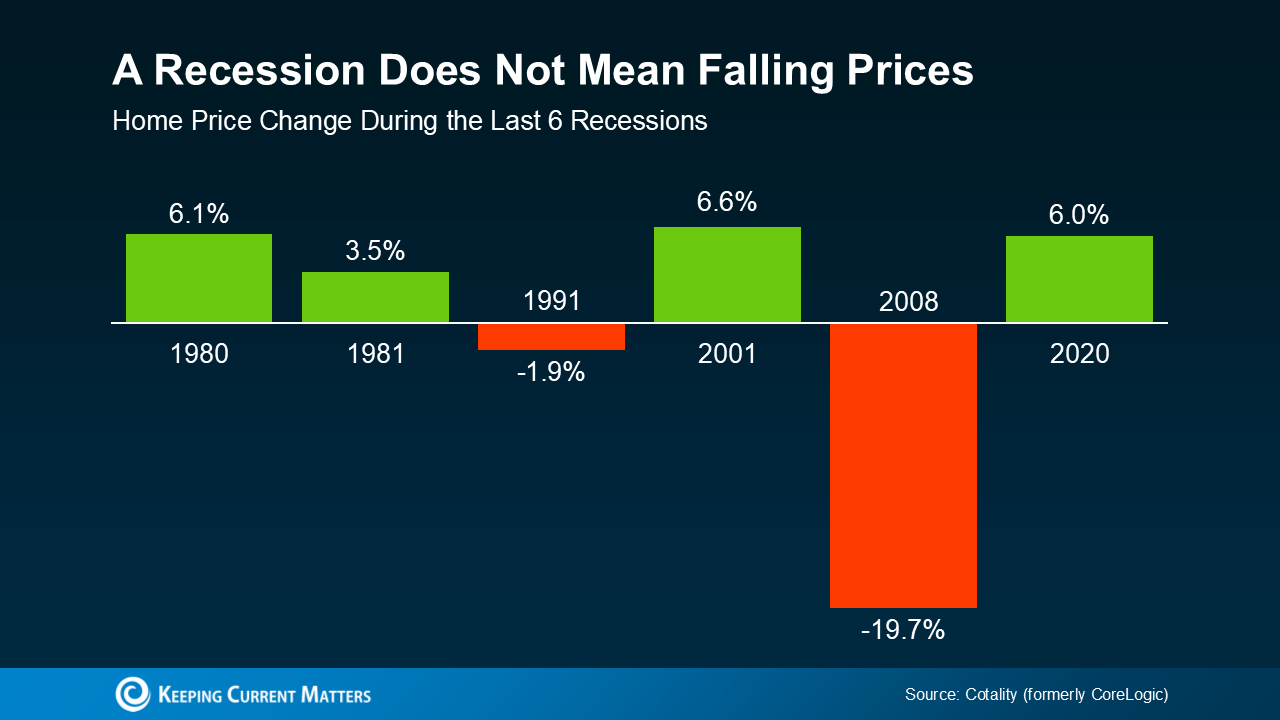

The first is often true—rates tend to fall in slowdowns as the Fed eases. But don’t count on falling home prices. According to data from Cotality (formerly CoreLogic), home prices actually rose in four of the last six U.S. recessions. And there’s some truth to the idea that a recession could bring about lower mortgage rates. History shows mortgage rates usually drop during economic slowdowns. That’s not guaranteed – but it is a common pattern. Looking at data from the last six recessions, you can see mortgage rates fell each time (see graph below):

While buyers often equate recession with discount real estate, it’s the exception—not the rule—that prices fall sharply (as in 2008). Today’s shortage of homes keeps prices from tanking, even amid economic slowdowns.

🛡️ Why Homes Usually Hold Value

-

Inventory shortages: With more buyers than sellers, prices stay elevated.

-

Recession dynamics: Mortgage rates fall, but sellers are less pressured to offload, limiting price dips.

-

Historical precedents: Only one recent recession saw steep price drops—2008.

Robert Frick of Navy Federal captures it well:

“Hopes that an economic slowdown will depress housing prices are wishful thinking at this point…”

According to data from Cotality (formerly CoreLogic), home prices went up in four of the last six recessions (see graph below)

💡 Broader Financial Context

Current financial experts are urging caution:

-

Business Insider highlights that uncertain conditions (tariffs, inflation, policy shifts) mean “stay put” is often advice for big decisions—housing included.

-

MarketWatch recommends building a 6–12 month emergency fund, keeping housing costs below 28% of income, and recalibrating investments for your life stage.

Other reputable sources (Washington Post, Time) echo the same: reduce debt, boost savings, and avoid making major purchases without strong financial protection and purpose.

🏡 Bottom Line: Move Sooner—If It Makes Sense for You

-

Waiting for rates? Could pay off—but timing is unpredictable.

-

Waiting for prices? Risky: the housing stock is tight, and prices don’t typically drop sharply.

-

What really matters? Your personal situation: job security, emergency funds, housing needs, and long-term plans.

If you’re ready—financially and in life—it might make more sense to act now than wait for a recession that may not deliver what you hope.

✅ Tips for Moving with Confidence

-

Secure your financial foundation

-

Build or maintain an emergency fund (6–12 months horizon).

-

Avoid over-stretching on housing costs—try to keep mortgage or rent under ~28% of gross income.

-

-

Collaborate with a trusted agent

-

Focus on market realities, not speculation.

-

Look at local trends: Are inventory shortages easing? Are supply/demand levels stable?

-

-

Strategize mortgage moves

-

If rates do drop post-purchase, refinancing could be a smart move—but don’t wait in hopes of hitting a perfect low.

-

Lock in when you can; be ready to revisit rates later.

-

-

Think long-term

-

Buying and selling homes are milestone events—not market games.

-

Focus on your personal needs, not timing the market.

-

✳️ Final Word

Don’t let fear or wishful thinking postpone your next move. Healthy recession talk isn’t a clear signal to delay—it’s a reminder to ground your decisions in your financial reality. If your budget, job, and life story align, now may be the smarter time to act—even in the face of economic uncertainty.