Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

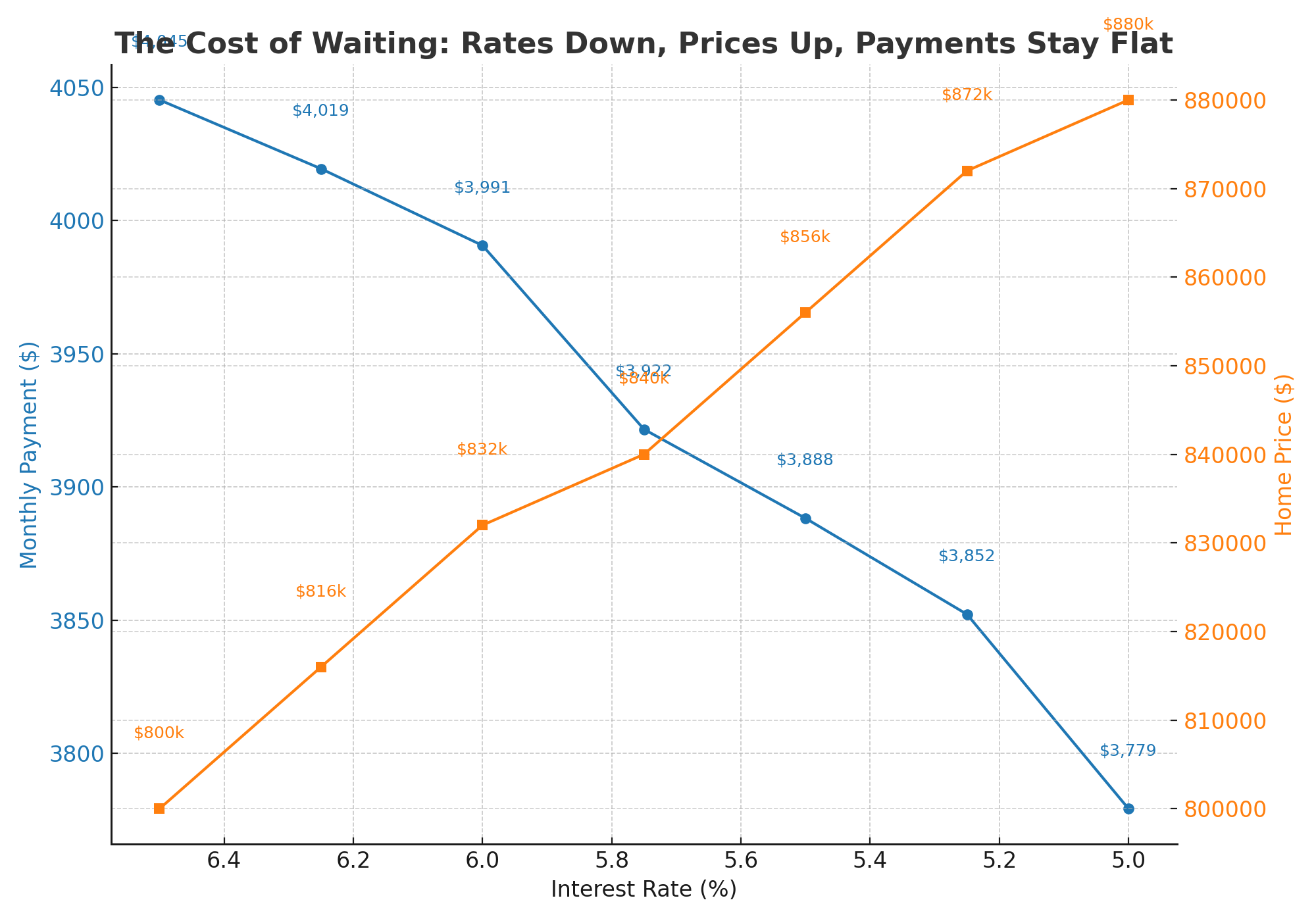

Mortgage rates have been on the move lately, and I have had many buyers asking the same question: should I buy now or wait for rates to drop? On the surface, waiting for a lower interest rate feels like the smart play. But in today’s market, where home values continue to rise when rates fall, the cost of waiting may surprise you. Let’s break it down:

Scenario 1: Buying Now

-

Home price: $800,000

-

Down payment (20%): $160,000

-

Loan amount: $640,000

-

Rate: 6.13%

Estimated monthly principal and interest payment: about $3,880.

Scenario 2: Waiting for a Lower Rate

Now imagine rates improve to 5.5%. Sounds great, right? But when rates fall, competition increases. More buyers flood the market, home prices will be pushed higher. A 7% price increase is realistic in that scenario based on what we saw in previous competitive markets.

-

New home price: $856,000

-

Down payment (20%): $171,200

-

Loan amount: $684,800

-

Rate: 5.5%

Estimated monthly principal and interest payment: about $3,887.

The Surprising Result

Even though the rate is lower in Scenario 2, the higher home price wipes out the savings. In fact, the monthly payment is nearly identical — slightly higher, in this case — and you end up borrowing more money overall.

Curious What This Could Mean for You?

Every buyer’s situation is unique, and timing the market is never simple. What we do know is that waiting for lower rates does not always mean a better deal, especially if prices rise in the meantime.

If you are curious how this plays out in your situation, I can run a personalized scenario based on your budget and goals. When you are ready to talk through the options, reach out and I will help you find the right move in today’s market.